University budgets are complex. This series breaks down that complexity.

Each week, UO Workplace News, the employee newsletter, publishes a new installment of UO Finances, a short, plain-language look at how the UO budget works: where money comes from, what drives costs, and what the numbers mean for our work. Those installments are collected here as a running reference.

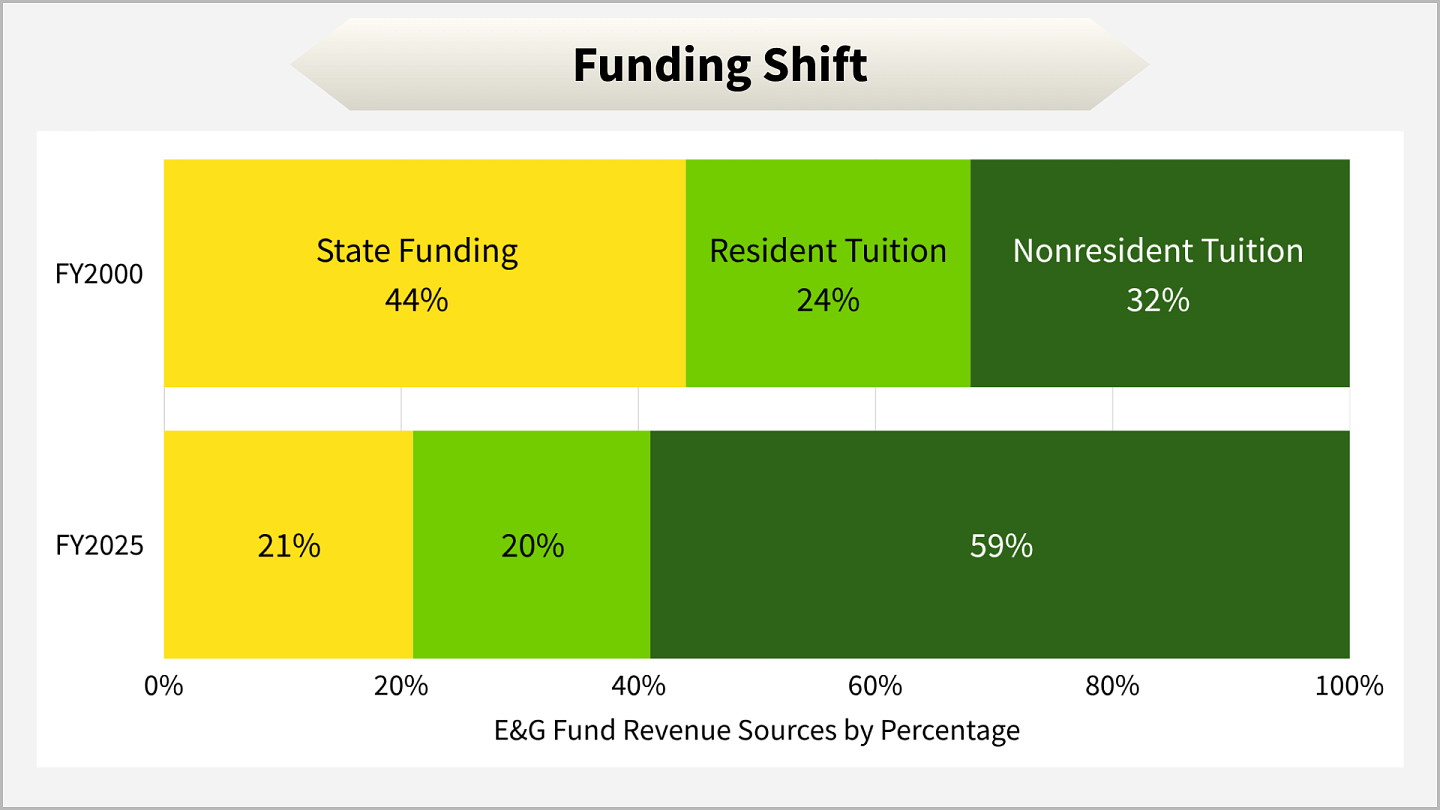

UO Finances 101: Where does the money come from?

- The UO is a complex organization and runs many operations. Those outside the core academic and administrative functions have separate funds. The core academic and administrative functions are within the primary operating budget, the Education & General (E&G) Fund.

- The largest revenue sources within the E&G fund are state appropriations and tuition with undergraduate tuition being the primary source.

- Over time, state appropriations have declined, increasing the university’s dependence on tuition, particularly nonresident tuition.

- If two students enroll—one paying in-state tuition and one paying out-of-state tuition—they both increase our enrollment. But they do not contribute the same amount of revenue. That’s why the mix of students matters, not just total enrollment.

The UO is increasingly reliant on tuition revenue, particularly nonresident undergraduate tuition.

UO Finances 102: Why can’t we just use that money?

The question behind the question: If UO receives major gifts, runs a successful athletics program, or holds a large endowment, why can’t those dollars help close the gap?

The answer has to do with how different kinds of university funds work.

Two kinds of funds

UO Finances 101 introduced an important idea: the university doesn’t operate from a single source of money. Instead, it has multiple funds.

- Unrestricted funds can be directed toward general operations, including salaries, utilities, and the day-to-day work of running a university.

Tuition and state appropriations are the main sources of unrestricted resources to support our core academic operations. Together, they make up over 90% of the Education and General (E&G) fund, the primary operating budget for core academic and administrative functions.

- Restricted funds must be used for a specific purpose defined by the source of funds.

A donor, a grant, or other contractual agreement sets the terms by which the university agrees to use the funds. In the case of endowments, often the funds themselves cannot be used, only the returns. The university is obligated to honor those agreements.

The takeaway

Most of the money people imagine might help is restricted, like endowed funds in the UO Foundation or funds for capital construction projects from donors or the state bond proceeds.

UO Finances 201: Where does the money go?

On the expense side, the biggest category is compensation and benefits

About 79% of the Education and General (E&G) fund expenses go toward total compensation packages for faculty, staff, and other employees. Total compensation includes wages and benefits such as health insurance, retirement savings, tuition benefits, and paid time off for employees.

This reflects that universities are people-centered organizations. We rely on and invest in people who teach our students, conduct cutting-edge research, provide student services, administer our systems, and maintain our facilities.

Other institutional expenses covered by the E&G fund are for supplies and services that support us every day, such as utilities, leases, travel, and debt service on academic buildings. Many of these are structural, recurring expenses that cannot be meaningfully reduced without reducing services to campuses.

The takeaway

The vast majority of university spending in the E&G fund supports recurring investments in people and essential systems. This gives us limited flexibility in how the university adjusts its budget when expenses outpace revenue and makes it difficult to change quickly—even as costs continue to rise over time.

Education and General Fund Context

Characteristics

- Approximately $708 million in revenue.

- 77% funded with tuition revenue.

- Funds the majority of activity in schools, colleges, and administrative units.

- 79% invested in people

Recent History

- FY26: $29.2 million structural budget reduction addressed an imbalance due to costs growing faster than revenues

- FY21-FY25: Balanced budget due to:

- Action taken to mitigate the impact of COVID-19

- Higher Education Emergency Relief Funds received for lost revenue funding

- Staffing challenges/compensation cost one-time savings

- FY20: $7.6 million deficit

- FY19: $11.5 million deficit

- FY16, FY17, and FY18: Balanced due to state investments, tuition increases and budget cuts

Key concepts about UO expenses

Not all expenses have the same long-term impact.

- One-time expenses happen once and do not repeat, such as a major equipment purchase or a short-term project.

- Ongoing expenses continue year after year, like salaries, benefits, utilities, and routine operations; often, these grow over time.

This distinction matters because ongoing costs require sustainable funding. Using one-time funds to cover ongoing expenses can create future budget gaps when those funds are no longer available.

Most spending is for ongoing commitments.

A large share of the university’s expenses are ongoing, or recurring, costs that the university is committed to over the long-term, unless structural changes are made. These include things like salaries, employee benefits, debt payments on academic buildings, utilities and long-term service agreements for things like core software systems. Recurring costs do not easily change from year to year.

Recurring expenses tend to increase over time.

University costs don’t stay the same year to year—they tend to grow. Several factors contribute to this:

- Compensation and benefits: Salaries may increase over time due to collective bargaining agreements or pay plan changes for unrepresented employees. Benefit costs, especially healthcare, also tend to rise.

- Inflation: The cost of goods and services—utilities, supplies, equipment, and construction—generally increases over time.

- Maintaining infrastructure and technology: Classroom technology, utility infrastructure, software systems, and property maintenance require ongoing investment to remain safe, functional, and effective.

- Expectations and requirements: Student needs, regulatory requirements, and standards can evolve, sometimes adding new costs.

Because these services are ongoing, expenses can increase even when the university is not expanding programs, unless actions are taken to become more efficient or reduce the scope of services offered.

UO Finances 301: What Does It Mean to Have a Balanced Budget?

It is simple and straightforward, but worth stating clearly when discussing the E&G budget:

- When revenue exceeds expenses, the university has a surplus of funds that can be used to invest in people, programs, services, etc;

- When expenses exceed revenue, the university has a budget deficit that must be addressed to secure its future; and

- The university maintains reserves as one-time buffers to sustain our programs, infrastructure, and people during short periods when expenses exceed revenues.

We must spend within our means

The principles of UO budgeting are very similar to those we all use in managing our own household budgets. We cannot spend more than we bring in. It is critical to have an emergency savings account for the unexpected, and expenses exceeding revenues cannot be sustained for long.

Responsible budgeting and financial management include understanding the size of our revenues and how fast they are growing, the size of our expenses and how fast they are growing, and the size of our reserves, which can help us navigate through challenging times.

Fiscal Year Fact:

In our E&G fund, revenues are expected to roughly balance with our expenses during FY2026. This is after undergoing budget reductions this year. Our E&G fund reserves represent just under nine weeks, a little less than a term, of operating expenses as of the second quarter of FY2026.

Small changes have big impacts

Expenses are ongoing and tend to increase over time. Most expenses, about 79%, in the E&G budget are related to compensation and benefits. Most revenues come from tuition, about 77% in the E&G budget. Growth in revenues are predicated on growing enrollment and, in particular, growing enrollment of nonresident students. Because compensation-related expenses and tuition revenues are in such a close balance, it means that the E&G budget is sensitive to even relatively small shifts in enrollment and tuition revenue or changes in compensation and benefits costs.

When revenue growth does not keep pace with increasing expense growth, a structural budget deficit results.

UO Finances 401: Why is higher education facing new financial pressures?

Higher education is entering one of the most financially challenging periods in decades, and the University of Oregon is no exception.

The collective pressure from a shrinking enrollment pipeline, increased competition, rising labor and operating costs, federal funding uncertainty, and declining public investment is forcing universities across the country to make difficult financial decisions.

The pressures at a glance

- Shrinking enrollment pipeline: National demographic trends point to fewer high school graduates over the next decade, particularly in the Pacific Northwest, reducing the number of traditional college-aged students entering higher education.

"U.S. Schools Face a Crisis as the Number of Children Drops," The New York Times, 2026.

"Knocking at the College Door: Projections of High School Graduates," Western Interstate Commission for Higher Education, 2024.

- Increased competition: Universities are offering larger financial aid packages, expanding student services, and increasing recruitment efforts to compete more aggressively for a smaller pool of students.

"The Enrollment Cliff: How Fewer Applicants Are Reshaping Higher Education," Forbes, 2025.

- Rising labor and operating costs: Compensation, healthcare, retirement obligations, utilities, technology, and insurance costs continue to rise even as many universities face limited revenue growth.

"Higher Education’s Uncertain Fiscal Future," Pew Charitable Trusts, 2025.

- Federal funding uncertainty: Research universities face growing uncertainty around federal grants and indirect cost recovery, creating challenges for research activity, innovation, and the infrastructure that supports them..

"NIH Funding Cuts Could Have Ripple Effects on College-Town Economies," The Chronicle of Higher Education, 2025.

- Declining public investment: Over time, public universities have received a smaller share of operating support from states, increasing dependence on tuition and other self-generated revenue, particularly in states with historically lower public funding levels for higher education.

"State Funding Update: The Fiscal and Political Crossroads Facing Public Higher Education," National Education Association, 2025.

"Opinion: An investment in higher education is an investment in Oregon’s economy," The Oregonian, 2025.

Impacts at UO

These pressures are not theoretical and present harsh realities. Like many universities nationwide, the UO is navigating significant financial challenges. The impacts of these challenges — and the university’s efforts to respond through careful fiscal stewardship and strategic decision-making — are described throughout the Financial Outlook section of this website.

The takeaway

Understanding the broader forces shaping higher education helps explain why universities across the country are reevaluating budgets and making difficult decisions.

The UO is not alone in confronting these pressures. And like many universities, it is working to balance financial realities with its commitments to students, faculty, staff, research, and the broader public mission of higher education.